Although NFTs have been around for quite a few years now, they’ve only now gained traction. In fact, they’ve become something of a fad where everyone wants to get in on the action.

The only thing that’s stopping most people is the confusion that surrounds them. For most people, the world of NFTs and crypto, i.e., blockchain technology, is bewildering. But when it comes to NFT, you don’t need to dig too deep to get started. Just the basics right and you’re good to go. Of course, as you’ll start, you’ll find that there is a lot to explore. But it’s best not to let the complexities and vastness of the subject daunt you.

Taking things slow is the best way to go. Here’s a little crash course for you.

What are NFTs?

NFTs are non-fungible tokens minted on, mostly Ethereum, but also other blockchains.

There are a lot of terms to unpack here. Firstly, if an item is fungible, it means that it is interchangeable. For example, a $10 note is interchangeable with another $10 note or two $5 notes. But an NFT is not. An NFT is a unique, non-interchangeable item.

The scope for what item can be an NFT is too wide. Although they’re most popular for digital art, items sold as NFTs include video clips, music files, memes, GIFs, tweets (yes, you heard it right). They’re also becoming increasingly popular for in-game items for video games or collectibles like pet rocks.

A few more items where NFTs are seeing practical usage include limited sneaker runs, event tickets, and even online essays.

You could either sell your own NFTs or become owners of NFTs by buying them. When you buy an NFT, the token acts as a certificate of authenticity. Anyone can verify that you own the NFT from the public ledger.

Explained: Minting an NFT

Seeing that anything can be an NFT, how does your digital art or other items actually come to be an NFT? Do you just create your item and tell people that it’s now an NFT? Of course not!

Any item becomes an NFT through the process of minting. To convert an item into an NFT, it has to become part of the blockchain ledger.

Blockchain is a publically distributed, decentralized ledger managed by a peer-to-peer network. There’s no centralized authority responsible for maintaining it. Instead, miners are responsible for adding new blocks to the blockchain.

Each block in the blockchain contains a cryptographic hash of the previous block, a timestamp, and the transaction data. Since the blocks are connected to previous blocks, modifying them is impossible without modifying all subsequent blocks in the chain. This property keeps the blockchain secure and safe from manipulation.

When you mint an NFT, the digital asset becomes a part of the blockchain. So, if you’re using the Ethereum blockchain to mint your NFT, it will become a part of the public ledger. And once that happens, you cannot modify it.

One uses a lot of energy to mint an NFT, i.e., to add it to the blockchain. Miners spend this energy in form of huge electricity bills that rack up when they solve complex puzzles to be able to add a block to the ledger. This huge energy spending is the reason blockchain is so heavily criticized.

Now, NFT creators pay for this energy spent in form of gas fees on the Ethereum blockchain. To mint an NFT, creators must pay a network fee which is ironically called gas fees. The gas fee fluctuates depending on the demand and usage of the network. As NFTs are trending right now and Ethereum is quite in demand, gas fees on the blockchain can be around $100-140.

Once you pay the gas fees, the NFT is minted.

Process for Minting an NFT

Here’s what the procedure looks like:

- Create a digital wallet of your choice

- Link that wallet to an NFT marketplace you like

- Add some ETH (Ethereum currency) to your wallet

- Upload the file to the marketplace and fill other details like price or type of auction, name and descriptiom for the file, etc.

- Double-check the details as you can’t modify them later

- Finally, click the Create button or its equivalent depending on the marketplace

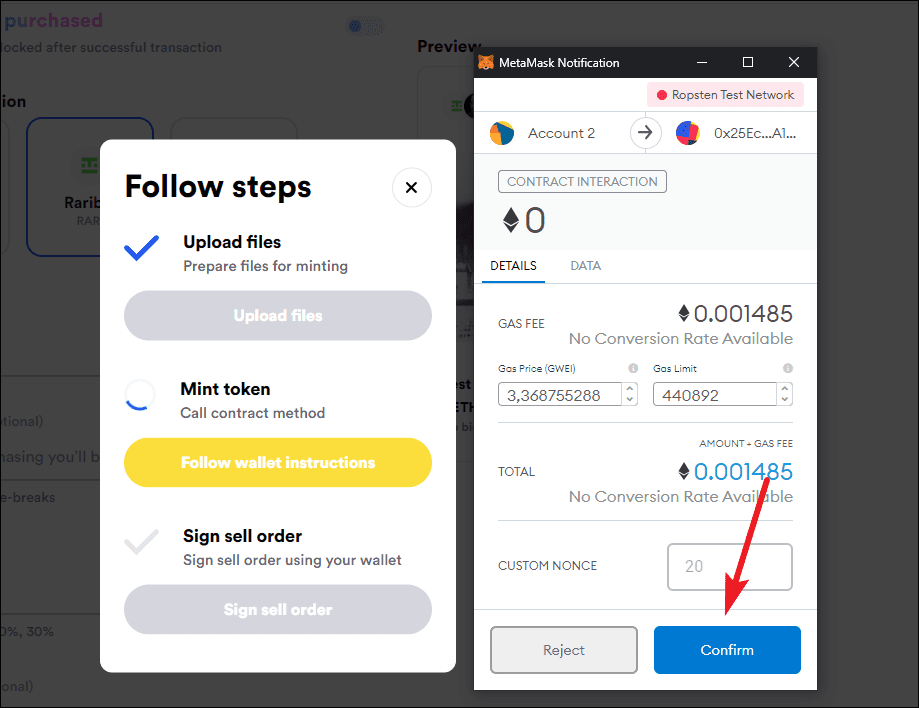

- Once you do that, the file is first uploaded to the IPFS (InterPlanetary File System)

- Then, the minting process starts. You’d get the request to pay the gas fees in your wallet.

- While all this is happening, you still have a chance to cancel. But once you confirm, the NFT is minted as soon as you pay the fee.

- Then, you’d get an additional signing request in your wallet to authorize the selling of the NFT. If you cancel now, the NFT will stay in your wallet until you decide to sell it.

👉Here’s a complete guide that’ll take you from understanding all aspects of NFT to creating a digital wallet and minting your first NFT.

When you mint the NFT, it is mapped to a token on the blockchain where it’ll live forever while the file itself is hosted on the IPFS. You cannot modify the NFT or delete it simply.

What you can do is burn the NFT which costs you gas fees again. Burning the NFT essentially deletes or removes it from the blockchain, and this process is irreversible.

So Does Lazy Minting Count as Minting?

Rarible, one of the most accessible NFT marketplaces, has introduced a new option to make NFTs more accessible for everyone. As the gas fees are too high, not all creators can pay it. Lazy Minting gives them the option to not create an NFT without paying the gas fees.

The gas fee is paid by the buyer instead. So, how is the NFT minted without paying the gas fee? The answer is that it isn’t.

The item that you want to turn into an NFT doesn’t even become an NFT until someone buys it. Rarible instead stores the file on the IPFS and delays the minting process. But the item is available on the marketplace like any other NFT. And just like any other NFT, you can sell it at a fixed price, or auction it off in timed or unlimited auctions.

When someone wants to buy the item, they pay the gas fees along with the price of the NFT. Once they pay the gas fees, the NFT is first minted in your wallet and then automatically transferred to the new owner’s wallet.

So, if no one buys your item, it is never minted as an NFT.

There you go. Hopefully, now you know what does it mean to mint an NFT. Now, go on and mint your first NFT.