This has been the year of NFTs. They are everywhere; Collins’ dictionary even named “NFT” the word of the year. Naturally, they’re piquing everyone’s curiosity.

They seem like the most idyllic thing on the internet right now – create something, sell it as an NFT and get rich overnight. But when you dive head-on into the NFT world, you’ll find that things aren’t as simple as any other fad on the internet. NFTs aren’t just a way to sell your art to strangers on the internet and make millions of dollars. There are too many crevices to fall into. But the one discovery that eventually takes down the rose-colored glasses from everyone’s eyes is the gas fees.

Those who have dipped their toes even slightly into the NFT waters know what we’re talking about. But the total newbies won’t. Still, you might have heard of the steep cost of creating, or selling NFTs and wondered what all that’s about? The one thing to come to mind is that maybe the huge costs must be due to the rising price of the crypto coin Ether. We’re here to debunk your misconceptions and help you separate fiction from truth.

NFTs: A Quick Explainer

NFTs (non-fungible tokens) are unique tokens that represent ownership of mostly digital, but sometimes physical, assets. They live and breathe on the blockchain – the token, that is. The file that you’re making into an NFT, on the other hand, is mostly stored on an IPFS (decentralized storage) for most blockchains. NFT can be thought of as a certificate of ownership for the digital asset.

Even though there are many blockchains in existence and many more appearing fast, the most popular in the NFT landscape is Ethereum. You can say Ethereum is to NFTs what Bitcoin is to cryptocurrency. It rules the NFT world right now.

So, can anyone hop onto Ethereum and make NFTs? Just kidding, you don’t hop onto Ethereum to make NFTs. You hop onto one of the NFT marketplaces that support the Ethereum blockchain and mint your NFTs there.

👉 We have a complete guide on how to mint NFTs that you can check out.

For using the Ethereum blockchain, you pay an amount that is known as gas fees. Gas Fee is paid in Ether (symbol: ETH) – Ethereum’s native cryptocurrency.

What’s the deal with Gas Fees?

To understand that, you must understand how NFT transactions, or transactions in general, on a blockchain work. At least, some of it. We can’t explain it in its entirety, of course; that’s a deep ocean.

Blockchains are decentralized ledgers that are maintained by a peer-to-peer network instead of a central server. They record information about transactions in blocks. To record information in a block, miners have to mine a block, validate the transaction and then add it to the block.

Ethereum uses a proof-of-work consensus algorithm to mine blocks. A proof-of-work algorithm requires the miners to perform huge computations to record a transaction. These computations consume a considerable amount of energy, and that’s where the gas fee comes in.

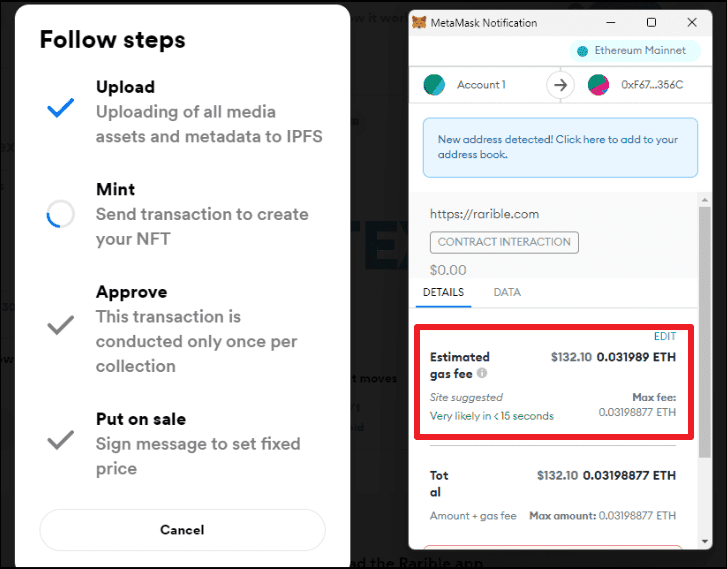

Since energy is required to carry out a transaction, you must pay for it. The gas fee is required not just to mint an NFT but to sell it too, as it’s basically a fee you pay to carry out a transaction on the blockchain. The gas fee has to be paid even to accept bids to sell your NFT. Once the gas fee is paid and the transaction is completed, it’s irreversible. It permanently becomes part of the blockchain. Even to delete your NFT from the blockchain (known as burning), you must pay a further gas fee.

The gas fee is never fixed and depends on the network usage. If the network wasn’t being used at all, the gas fee would be very low. but when the network is in high demand, the gas fee increases.

The Ethereum network is very popular these days and that reflects in the high gas fees you have to pay. High gas fees on Ethereum also result from its scalability issues and the proof-of-work consensus algorithm.

Scalability issues

Scalability issues have long been Ethereum’s Achilles Heel. Ethereum has employed Sharding, a technique that aims to address this issue, but so far, it hasn’t been too successful.

Whenever there are too many transactions on the network, a huge bottleneck is created. A recent example: TIME magazine’s NFT. TIME magazine launched over 4000 NFTs on Ethereum, priced at 0.1 ETH (around $300 at the time).

But the NFTs were released at a certain time, and users flooded to buy them. There were more than 4000 transactions on Ethereum at the same time.

The bottleneck that happened resulted in huge gas fees. Other than that, to prioritize their transactions over others, users can pay miners a “priority fee” which is sort of like a bribe.

Due to this, the gas fees for the whole fiasco was skyrocketed.

Proof-of-Work as a Contributor to Gas Fees

Proof-of-work algorithm is solely responsible for the huge gas fees on the Ethereum network. The proof-of-work algorithm is heavily energy-consuming, which is by design. It keeps the system secure. But it has huge impacts, on the environment as well as gas fees.

There’s an alternative – Proof-of-stake. A few other blockchains already use it, and Etehreum would be transitioning to it in the coming time. WIth proof-of-stake, Ethereum’s energy consumption would drop almost by 99%.

A proof-of-stake system requires the network validators to have some stake in the system, instead of proving their work by performing complex computations.

So, you see. The gas price, and hence the price to mint an NFT, has nothing to do with the increasing or decreasing price of the Ether cryptocurrency. It only depends on the network usage. You can use a tool like Rarible Analytics to determine when the network usage is low to avoid too high fees. You can also use blockchains other than Ethereum that have fewer gas fees.